Under current Virginia law, liability policy limits can only be revealed to a plaintiff’s attorney within limited circumstances, unless a lawsuit is filed.

By Matthew E. Bass, attorney at Burnett & Williams P.C., Loudoun, Fairfax, and Northern Virginia

When someone is seriously injured in a car crash, one critical aspect for a Virginia personal injury attorney to investigate is what kind of liability insurance coverage limits will be available to pay on the claim. [i] One may assume that the liable (at-fault) party’s insurance company must simply disclose the available limits of liability insurance upon request from the injured party’s attorney. However, that is not the case under Virginia law.

Thanks to a law passed in 2008, for the last decade or so the law has required that unless a lawsuit is filed, an injured person’s lawyer in Virginia can only discover the available limits of liability insurance once the total of their client’s medical bills and lost wages [ii] meet or exceed $12,500. But why is $12,500 the threshold?

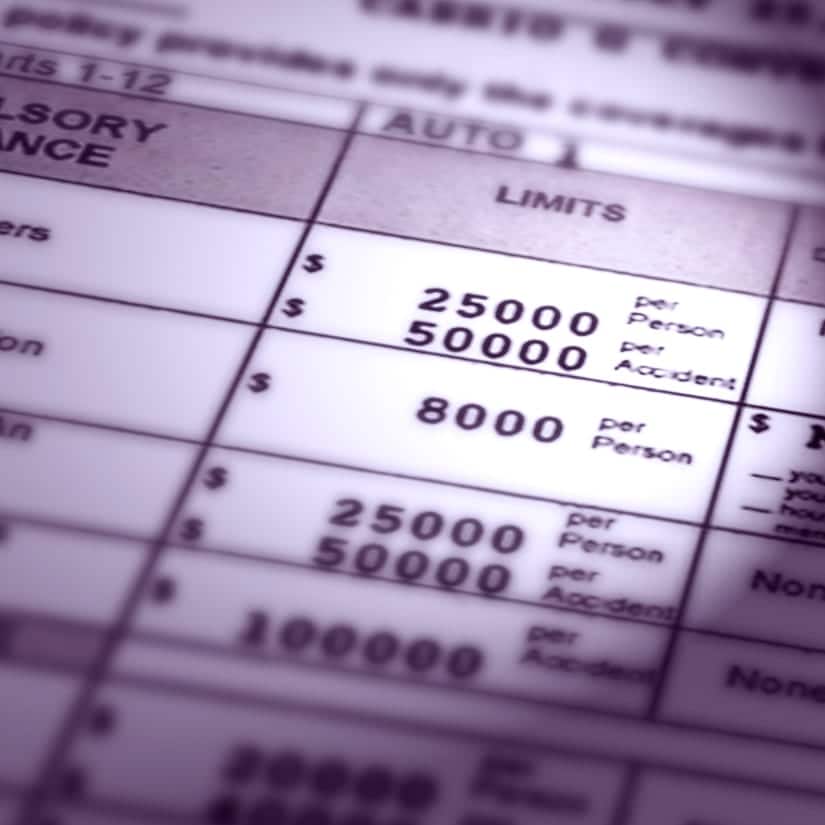

Part of the answer may be that $12,500 is exactly half of the required minimum level of liability insurance in Virginia, which is $25,000 per injured person, up to a maximum of $50,000 per accident. [iii] The thinking behind the 2008 law requiring this disclosure was that plaintiff lawyers needed to know whether underinsured motorist coverage — or UIM coverage — would be implicated, which is likely in cases with minimum levels of liability coverage ($25,000) and at least $12,500 in medical bills and lost wages. And, practically speaking, those cases with medical bills and lost wages of at least $12,500 might resolve more quickly once the injured person’s lawyer finds out they are dealing with minimum policy limits.

In 2018, the law in Virginia was amended to additionally allow for discovery of liability policy limits if the at-fault party was convicted of DUI (or similar offenses) and the injured person’s injuries arose from the same incident resulting in that conviction, without regard for the dollar amount of medical bills and lost wages. The rationale behind this more recent change in the law is that, in certain circumstances, an intoxicated driver who causes an injury may be liable for “punitive damages,” which punish them for their conduct, in addition to being responsible for medical bills, lost wages, and other specified damages permitted under Virginia law. Following the reasoning of the 2008 law regarding $12,500 in medical bills and lost wages, the idea is that UIM coverage may be triggered — or a liability case may resolve more quickly — if the liable party has been convicted of DUI and the injured person’s lawyer knows the available liability policy limits.

In a time of over-crowded dockets, underfunded court systems, and more personal injury cases (and cars, and people) than ever before, it’s easy to argue that expanded disclosure of liability policy limits — with the underlying goal of opening the door to available coverage limits and facilitating settlement prior to litigation — would be a valuable tool for Virginia personal injury plaintiffs’ attorneys. [iv] However, even with the plaintiff-friendly 2018 change to the law regarding discovery of liability policy limits, lawyers for injured persons in Virginia are still limited to just the two circumstances outlined above if they want to find out how much liability insurance is available without filing a lawsuit.

If you or someone you know has been injured by a drunk driver in Virginia, please contact the attorneys at Burnett & Williams at 703-777-1650.

i. For a more detailed discussion on another potential source of insurance coverage, underinsured motorist coverage (“UIM”), see our Burnett & Williams’ blogs about making sure you have adequate auto insurance — https://burnettwilliams.com/what-you-should-know-about-car-insurance-from-personal-injury-lawyers/ and https://burnettwilliams.com/auto-insurance-smarts/ — or schedule a time for one of our personal injury attorneys to give a brief presentation to you and your friends or colleagues on the topic by calling 703-777-1650.

ii. Visit www.burnettwilliams.com for a more detailed discussion on damages.

iii. In other words, if the liable party has minimum liability insurance coverage levels of $25,000 per person, $50,000 per accident (commonly known as “split limit”), the injured individual may only recover up to $25,000, and the liability insurance company is only responsible for a total of $50,000, regardless of how many people are injured in a single accident and the severity of their injuries.

iv. The author can’t help but wonder whether Virginia will ever see a day where insurance companies are required to simply disclose available liability policy limits after being notified of a claim.